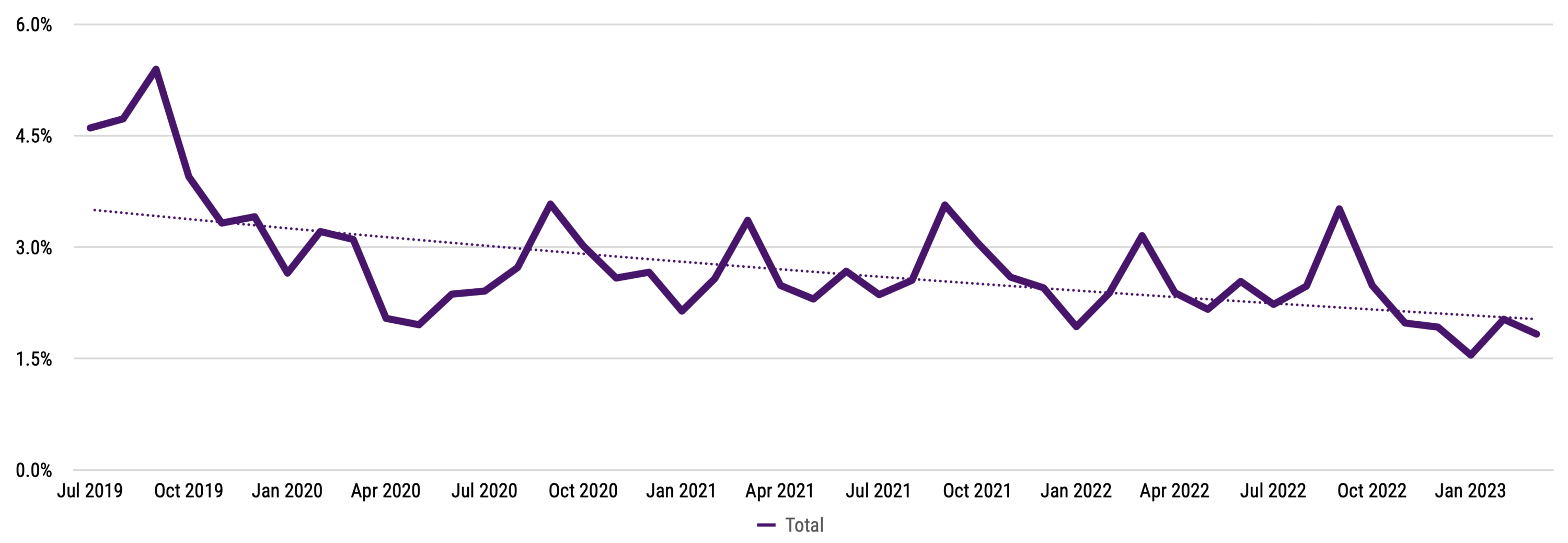

One of the biggest retail casualties of the pandemic has been the availability of new and refreshed products for consumers. Before the pandemic, new general merchandise products made up more than 5% of the market. Since then, that number has fallen to less than 2%.

Investment in new product development was understandably put on hold during the pandemic’s uncertainty. Most companies adjusted priorities to fulfill demand when consumer spending took an unexpected upward turn. Raw goods became a challenge, so that became the priority. When demand subsided, there was too much supply, and selling became the main concern — and still no significant focus on new products.

“Consumers proved their resilience during the pandemic, spending at unprecedented levels that continued despite escalating prices. Now they’re hungry for something new,” said Marshal Cohen, chief retail industry advisor for Circana. “That means retailers and manufacturers need to have something new to offer. The ongoing sales declines cause marketers to question whether they should focus on building something new or pricing product differently. The answer is: It’s time to do both.”

Across discretionary general merchandise and CPG, the trends in consumer spending and new product deficits in the marketplace have directional similarities, intensified by elevated prices. Compounding these consumer distractions is the economic news that continues to put vulnerability into the air.

It’s time to welcome new products and amplify newness in a big way to consumers. But it’s not solely about product innovation. Consumers respond to economic uncertainty by reevaluating their spending behavior, making it more important than ever to broadcast the value that your brand, your product, or your store brings to the consumer.

“Both the retail landscape and consumer behavior have changed dramatically over the past few years. Retail holiday sales surges are not reaching their traditional peaks,” said Don Unser, president of general merchandise and retail thought leadership for Circana. “Consumer tech, apparel, and other high-volume industries don’t consistently provide the same growth boost they once did. There is a real need for many manufacturers and retailers to shift the way they are thinking to create some spending elevation.”

Kristen Classi-Zummo, Industry Advisor

The apparel industry is in danger of finding itself back where it was in 2019, with bored consumers and out-of-control promotions. With immediate fashion needs met, purchase motivators will likely shift focus to two things: innovation and joy. Consumers will crave updated silhouettes, new performance features, and fresh colors that keep them both intrigued and excited.

However, the industry is currently experiencing the opposite: Only 19% of dollars spent on apparel in 2022 went to new styles, and that’s even lower than it was in 2019, shown by Retail Tracking Service point-of-sale data from Circana. Rather than intrigue, stagnation plagues the industry. This can be attributed to a pullback in innovation, including collaboration stifled by remote work, supply chain challenges, and erratic consumer demand.

Key takeaways:

For more on this topic, read Kristen Classi-Zummo’s article at Forbes.com.

Ben Arnold, Industry Analyst

The technology industry thrives on innovation, and consumers expect to be delighted whenever they invest in a new tech product. Understandably, product development and innovation in consumer electronics have been challenged over the past few years as the industry weathered the pandemic and addressed the many demand, supply, and cost challenges that followed. Technology sales are off to a slow start so far in 2023. (Revenue through the first 13 weeks of the year declined by 13%.) However, new products and novel feature and price combinations are resonating in the market.

Joe Derochowski, Industry Advisor

In 2020, 13% of small home appliances sales were from new products to the market. Compare that to 2022, when the share fell to just 8%. It’s clear that the business challenges presented by the pandemic meant creating new and innovative products was not prioritized as highly. These days, there’s a clear and renewed need for innovation – not only in the products sent to market, but also in the way those products are marketed and sold in stores.

Beth Goldstein, Industry Advisor

The share of U.S. footwear sales revenue generated by new items (defined as items released in that same year) fell to 17% in 2022 from 23% in 2019. Footwear is an industry for which iconic and classic styles are extremely important, so it’s understandable that the majority of sales would come from existing products. However, as with any fashion category, footwear trends and brand popularity are cyclical, so it is important to keep up the pipeline of fresh product to keep consumers interested.